Total Contribution Margin At The Break-Even Point

Margin At The Break-Even Point

Margin At The Break-Even Point

To calculate the wreck-even point in units use Margin At The Break-even Point factor (devices) = fixed charges ÷ (sales charge in line with the unit – Variable charges in step with the unit) or in sales bucks the use of the method: damage-Even factor (sales greenbacks) = constant costs ÷ Contribution Margin.

FreshBooks guide group individuals who haven’t licensed income tax or accounting specialists and can not provide recommendations in those areas, outdoor of supporting questions about FreshBooks. In case you want income tax recommendations please contact an accountant in your region Margin At The Break-Even Point.

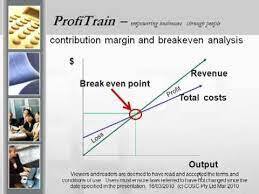

What is the smash-Even factor?

The wreck-even point is the point wherein a corporation’s revenues equal its charges. The calculation for the damage-even factor can be executed certainly one of the approaches; Margin At The Break-Even Pointone is to determine the number of devices that want to be offered, or the second one is quantity of income, in greenbacks, that want to happen.

The destroy-even point permits a corporation to realize while it, or certainly one of its products, will begin to be worthwhile. If an enterprise’s sales are under the smash-even point, then the enterprise is working at a loss. If it’s above, then it’s operating at earnings.

The way to Calculate ruin Even point in units

Fixed fees ÷ (sales fee in line with UNIT – VARIABLE fees consistent with UNIT)

Fixed fees – fixed expenses are ones that commonly do no longer change, or trade most effective slightly. Margin At The Break-Even Point Examples of constant prices for a business are month-to-month application expenses and lease.

Sales charge in step with Unit- this is how a good deal a company goes to charge customers for simply one of the goods that the calculation is being done for.

Variable prices in step with Unit- Variable charges are costs at once tied to the manufacturing of a product, like labor employed to make that product or substances used. Margin At The Break-Even Point Variable prices frequently ranges and are generally an organization’s largest cost.

Read more: Problems signing in to QuickBooks Online?

The calculation is as follows:

Total variable fees ÷ general units produced

Break-Even factor Examples

Permit’s display a couple of examples of a way to calculate the break-even factor.

Sam’s Sodas is a gentle drink producer within the Seattle vicinity. He’s thinking about introducing a new tender drink, known as Sam’s silly Soda. He wants to recognize what kind of effect this new drink will have on the company’s price range. Margin At The Break-Even Point So, he decides to calculate the spoil-even point, so that he and his management team can determine whether or not this new product may be worth the investment.

His accounting fees are as follows, for the primary month the product may be in manufacturing:

Fixed prices = $2,000 (general, for the month)

Variable prices =.Forty (in step with can produced)

Sales price = $1.50 (a can)

Calculating the damage-Even point in devices

Fixed prices ÷ (income charge in line with the unit – Variable fees in keeping with the unit)

$2000/($1.50 – $.40)

Or $2000/1.10

=1818 units

This means Sam needs to promote just over 1800 cans of the new soda in a month, to reach the damage-even factor.

Searching out sources that will help you manage your commercial enterprise for the duration of COVID-19?

Take a look at the FreshBooks COVID-19 useful resource Hub.

Calculating the wreck-Even factor in sales dollars

Constant expenses ÷ Contribution Margin

Constant charges

(See above)

Contribution Margin

Contribution Margin is the distinction between the fee of a product and what it prices to make that product.

The calculation is as follows:

(Sale charge according to unit – Variable fees in keeping with the unit)/Sale rate in step with unit

Wreck-Even point Examples

Let’s show a couple of examples of a way to calculate the ruin-even factor.

Sam’s Sodas is a smooth drink producer inside Seattle place. He’s thinking about introducing a brand new gentle drink, referred to as Sam’s silly Soda. He wants to understand what sort of impact this new drink will have on the corporation’s price range. So, he decides to calculate the smash-even point, so that he and his control crew can determine whether or not this new product might be worth the investment.

His accounting expenses are as follows, for the first month the product will be in manufacturing:

Constant prices = $2,000 (total, for the month)

Variable fees =.Forty (in line with can produced)

Sales rate = $1.50 (a can)

Calculating The damage-Even point in devices

Constant expenses ÷ (income charge per unit – Variable charges in step with the unit)

$2000/($1.50 – $.Forty)

Or $2000/1.10

=1818 units

This indicates Sam desires to sell just over 1800 cans of the new soda in a month, to attain the smash-even point.

Calculating The smash-Even factor in income dollars

Fixed prices ÷ Contribution Margin (sales rate according to unit – Variable charges according to the unit, with a resulting parent then divided with the aid of sales fee according to unit)

$2000/.7333=$2727

This indicates Sam’s crew desires to promote $2727 worth of Sam’s stupid Soda in that month, to interrupt even. Anything after that amount may be income for the employer.

To confirm this parent: you may take the 1818 gadgets from the primary calculation, and multiply that via the $1.50 sales charge, to get the $2727 amount.